Gold Loans in India: Why a ₹5 Lakh Crore Boom Changes How You Should Think About Gold

RBI data shows gold loans growing 125%+ YoY, the fastest of any credit segment. Here's what's driving India's gold monetization boom and what it means for your portfolio.

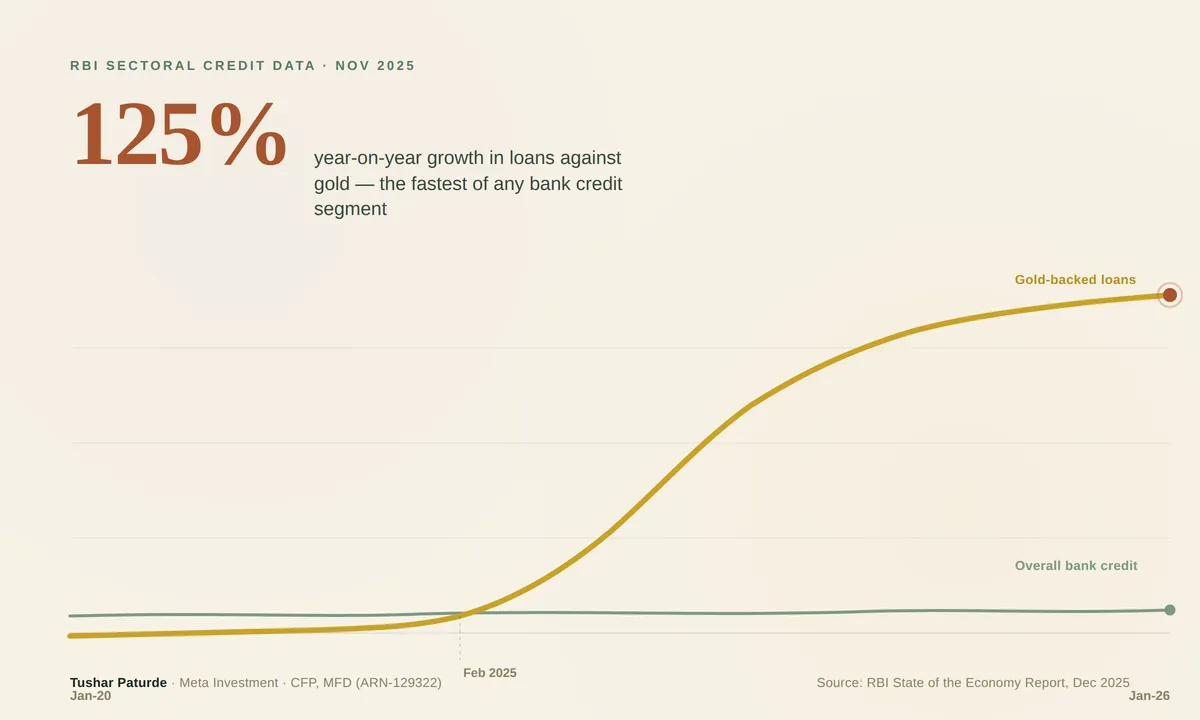

Indian households are no longer just buying gold and locking it away — they’re putting it to work. RBI data shows gold loans growing over 125% year-on-year, the fastest of any major bank credit segment. Here’s what the numbers actually say, why it’s happening now, and what it means for how you think about gold in your own portfolio.

Introduction

For generations, gold in an Indian household followed a predictable life cycle: bought for a wedding or festival, stored in a locker, and largely forgotten until the next family milestone. It sat there — valuable, but inert.

That pattern is breaking, and the scale of the shift is bigger than most people realise.

According to the Reserve Bank of India’s own sectoral credit data, loans against gold jewellery have been recording triple-digit year-on-year growth every single month since February 2025 — comfortably outpacing every other major retail credit category, including housing, vehicle loans, and credit cards. This isn’t a short-lived spike. It’s a structural shift in how Indian households are using one of their largest stores of wealth.

In this post, we’ll walk through what the data actually shows, why it’s happening now, and — more importantly — what it should change (and not change) about how you think about gold in your own financial plan.

The Data: How Big Is This, Really?

Let’s start with the numbers, straight from RBI’s reporting.

- Loan growth: Loans against gold jewellery grew over 125% year-on-year as of November 2025, against overall bank credit growth of roughly 11.5% in the same period. Gold loans were, by a wide margin, the fastest-growing credit segment in the banking system.

- Sustained, not a blip: RBI’s State of the Economy report (December 2025) confirms that gold-backed loans have posted triple-digit growth every month since February 2025 — nearly a full year of acceleration, not a one-quarter anomaly.

- The base has roughly 10x’d in six years: Outstanding bank credit against gold has gone from a few tens of thousands of crores to an estimated ₹3.5–4.9 lakh crore, depending on the data cut and reporting date used.

- Small base, outsized impact: Gold loans still account for less than 2% of total outstanding bank credit — but they contributed close to 12% of all incremental (new) lending in the system through November 2025. The base is small. The momentum is not.

Why Now? The Gold Price Connection

The single biggest driver isn’t a change in regulation or a sudden surge in financial distress — it’s gold prices.

24-karat gold in India climbed roughly 60–70% through 2025, moving from around ₹76,500 per 10 grams at the start of the year, crossing ₹1 lakh per 10g by April, and pushing past ₹1.3 lakh by year-end. By early 2026, prices had briefly touched all-time highs near ₹1.78 lakh per 10g.

Here’s the mechanism that matters: when the price of gold rises, the collateral value of the same piece of jewellery rises with it. A household that could borrow ₹2 lakh against a particular set of jewellery two years ago can now borrow significantly more against that exact same gold — without selling a single gram.

That’s the core insight behind the term “gold monetization.” Households aren’t liquidating their gold. They’re unlocking liquidity from it while keeping the asset itself — pledging it for working capital, business needs, emergencies, or consumption, and reclaiming it once the loan is repaid.

Why This Matters for the Economy — and for You

The Case for “Good”

There’s a genuine economic upside here. Gold sitting in a locker is, from an economic standpoint, dead capital — it earns nothing and contributes nothing to productive activity. When that gold gets pledged for a loan, the value locked inside it re-enters the economy as usable credit, while the household retains full ownership of the underlying asset.

Gold loans also tend to be:

- Cheaper than unsecured personal loans or credit cards, because they’re fully collateralized

- Faster to disburse, often within hours

- Less damaging to credit profile if structured and repaid sensibly, compared to revolving unsecured debt

The Case for Caution

RBI itself has flagged the segment for monitoring, not because the absolute exposure is dangerous today, but because of what happens if the trend reverses.

- Price sensitivity: Loans sized against a high gold price become harder to service — and the collateral cover thins — if prices correct sharply. A 60-70% rally followed by a meaningful pullback is not a hypothetical; it’s happened before in gold cycles.

- Regulatory tightening already underway: RBI’s 2025 rules cap loan-to-value (LTV) at 75% for gold loans above ₹5 lakh (smaller loans up to ₹2.5 lakh can still go up to 85% LTV), and lenders must now issue a Gold Purity Certificate detailing weight, purity, and valuation. These rules exist precisely because rapid growth in any lending category invites scrutiny.

- Behavioral risk: Easy access to liquidity against an appreciating asset can tempt households into borrowing for consumption rather than genuine need — turning a productive financial tool into a habit that erodes the very wealth the gold represents.

What This Means for Your Own Portfolio

This trend isn’t really a signal to rush out and pledge your gold. It’s a signal to rethink how you categorize gold within your financial plan.

| Old framing | New framing |

|---|---|

| Gold is a one-time purchase for occasions | Gold is a working asset class with utility and return potential |

| Gold = physical jewellery only | Gold = jewellery, Sovereign Gold Bonds (SGBs), gold ETFs, EGR (Electronic Gold Receipts) , or gold mutual funds — each with different liquidity and tax treatment |

| Gold sits idle until sold | Gold can serve as a collateral-backed liquidity buffer without being sold |

| “How much gold do I own?” | “What role does gold play in my overall asset allocation — hedge, liquidity reserve, or growth bet?” |

A few practical questions worth sitting with:

- If you hold physical gold, do you know its current market value, and have you considered whether SGBs, EGR or gold funds might serve the same purpose with better tax efficiency and no storage risk?

- If you’re considering a gold loan, is it funding something productive (business capital, a genuine emergency) or is it substituting for disciplined saving and emergency fund planning?

- In your broader asset allocation, is gold sized appropriately as a diversifier — typically a modest single-digit to low-teens percentage for most investors — rather than as an outsized concentration?

Key Takeaways

- Gold loans grew 125%+ year-on-year as of November 2025 — the fastest growth among all major bank credit categories, against ~11.5% overall credit growth.

- This has been sustained triple-digit growth every month since February 2025, not a one-off spike.

- Gold loans remain under 2% of total bank credit but are driving close to 12% of all new lending — a small base with outsized momentum.

- The primary driver is the 60-70% rise in gold prices through 2025, which inflated the collateral value households can borrow against.

- RBI has introduced LTV caps and purity certification rules in response to the segment’s rapid growth, signalling it’s being watched closely.

- For individual investors, the real takeaway is to view gold as a working asset class within a broader allocation strategy — not just a locker item, and not just a loan source either.

Conclusion

Gold’s transformation from a dormant family asset into an active, liquid financial instrument is one of the more underappreciated shifts in Indian household finance right now. The RBI data is unambiguous: this isn’t a marginal trend, it’s the fastest-moving segment in the entire credit system.

Whether that’s a positive development for your own finances depends entirely on how deliberately you engage with it — as a tool for genuine liquidity needs and a well-sized part of your asset allocation, rather than as easy money against a rising price.

If you’d like to review how gold fits into your overall portfolio — whether through physical holdings, Sovereign Gold Bonds, or gold mutual funds — reach out for a conversation about your specific allocation and goals.

Interested in Investing? Connect with Meta Investment

Meta Investment is a financial product distribution and services firm. If you'd like to explore whether a financial product is the right fit for your portfolio, our team will walk you through the details, help you assess suitability, and guide you through the onboarding process.

Tushar Paturde is a Certified Financial Planner (CFP) and Founder of Meta Investment, an AMFI-registered Mutual Fund Distributor (ARN-129322) and PMS distribution partner (APMI APRN01448). Meta Investment is not a SEBI-registered Investment Adviser. This article is for general educational purposes only and does not constitute personalised investment advice. Mutual Fund investments are subject to market risks; please read all scheme-related documents carefully. Data referenced is sourced from the RBI’s State of the Economy report (December 2025) and related RBI credit data releases.

0

Market insights, straight to WhatsApp — when it matters

Mutual fund updates, SIP tips, and what's moving the market. No daily noise — only when there's something worth reading.

")