ICICI Pru Thematic Advantage Fund: What the Recategorization Means for You

ICICI Pru Thematic Advantage Fund (FOF) is being renamed and recategorized — here's what changes, what stays the same, and what investors should know.

If you’re invested in the ICICI Prudential Thematic Advantage Fund (FOF), you may have recently received communication about a significant change coming your way. Starting April 1, 2026, the scheme is being rechristened as the ICICI Prudential Aggressive Hybrid Active FOF.

At first glance, a name change and category shift can feel unsettling. But as you’ll see, this recategorization is largely a regulatory housekeeping exercise — one that actually expands the fund’s investment toolkit rather than curtailing it.

Let’s break down everything you need to know.

Why Is ICICI Pru Recategorizing This Fund?

On February 6, 2025, SEBI — through AMFI — introduced a new “Framework for launching Fund of Fund (FOF) schemes with multiple underlying funds.” This regulatory directive required all existing FOF schemes to align themselves with its provisions.

The ICICI Pru Thematic Advantage Fund, being a multi-theme FOF that actively rotates between sectors and themes, needed to be repositioned to comply with this framework. Rather than simply tweaking the name, ICICI Prudential has used this as an opportunity to enhance the scheme’s structural flexibility.

This is a SEBI-mandated recategorization, not a strategic overhaul. The fund house’s investment philosophy remains intact.

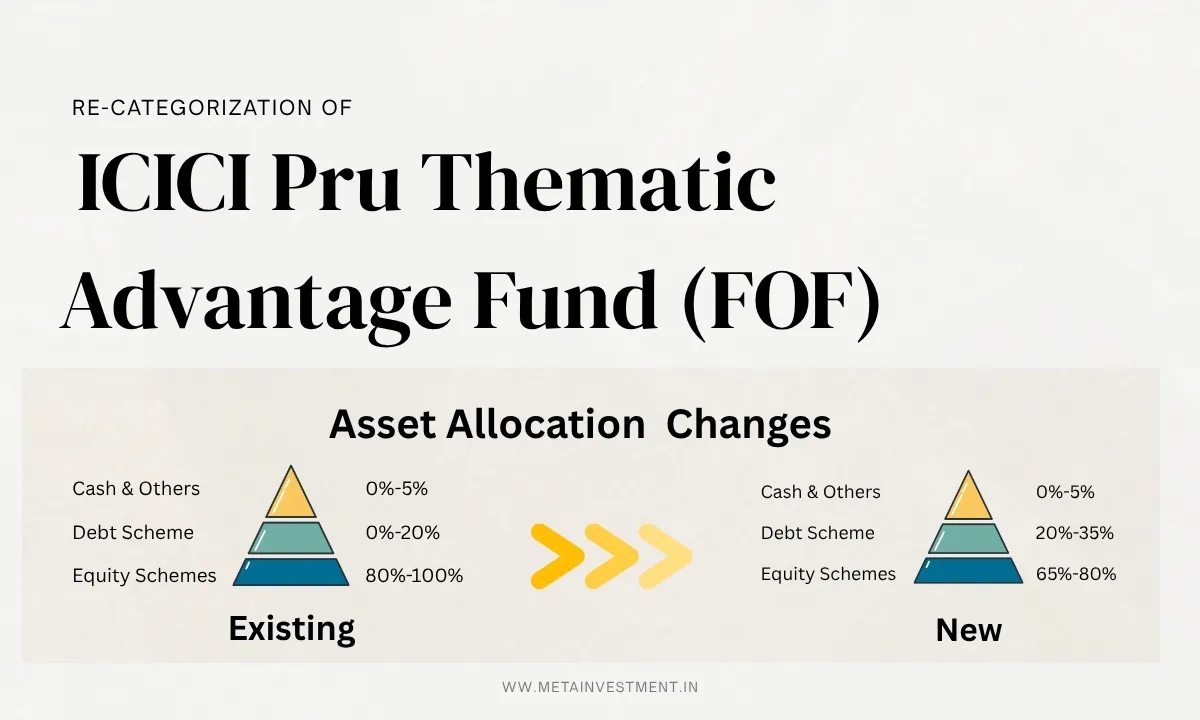

What Changes: The New Asset Allocation

The most tangible change is in the asset allocation mandate. Here’s a side-by-side comparison:

| Component | Existing Allocation | New Allocation |

|---|---|---|

| Equity Schemes (Sectoral + Thematic) | 80% – 100% | 65% – 80% |

| Debt Schemes | 0% – 20% | 20% – 35% |

| Cash & Others | 0% – 5% | 0% – 5% |

Under the new structure, the equity allocation floor shifts slightly from 80% to 65%, while the debt component gets a formal, mandatory floor of 20%. This makes the fund structurally more of a hybrid — hence the “Aggressive Hybrid Active FOF” label.

Alongside sectoral and thematic equity schemes, the fund can now also invest in market capitalization-based equity schemes (large cap, mid cap, small cap), giving the fund manager more tactical levers to work with.

What Stays the Same: The Core Strategy

Despite the name change, the soul of the scheme remains unchanged. Here’s what investors can continue to expect:

- Sector and theme rotation remains the primary growth engine. The fund will continue to actively move between sectors like banking, pharma, technology, FMCG, energy, and others based on market outlook.

- The fund retains full flexibility to take aggressive or defensive stances depending on the market environment.

- The 80% equity exposure (now as a target rather than a strict floor) ensures investors experience a similar level of growth orientation as before.

In practice, debt was never absent from this fund. Historical data shows the scheme has consistently held between 5% and 17% in debt and cash — so the formal 20% minimum is more of a regulatory acknowledgment of existing behaviour than a dramatic portfolio change.

Historical Portfolio: How the Fund Has Evolved

To understand the continuity of strategy, look at how the scheme’s underlying holdings have shifted over time:

| Underlying Scheme | Oct ‘21–Apr ‘22 | Aug ‘24–Dec ‘24 | May ‘25–Jun ‘25 | Feb ‘26 |

|---|---|---|---|---|

| Banking & Financial Services | 20% | 30% | 27% | 20% |

| Pharma Healthcare & Diagnostics | 19% | 25% | 13% | 17% |

| Technology | 6% | 7% | 12% | 22% |

| Bharat Consumption | 1% | 20% | 14% | 8% |

| Energy Opportunities | — | — | 10% | 19% |

| FMCG | 1% | 1% | 7% | 4% |

| Debt Schemes & Cash | 16% | 17% | 12% | 5% |

The fund has demonstrated its ability to rotate meaningfully — from heavy banking exposure in 2024 to a tech-heavy tilt by early 2026. This dynamism is the scheme’s core differentiator, and it is fully preserved post-recategorization.

New Opportunities Unlocked by the Reclassification

The recategorization isn’t just about compliance — it genuinely broadens what the fund can do:

-

Tactical mid and small cap exposure: The fund can now allocate to market cap-based equity schemes, allowing it to ride mid and small cap rallies without being constrained to only sectoral or thematic funds.

-

Structured debt exposure: A formal debt sleeve (20%–35%) gives the fund manager a buffer to protect capital during volatile periods, without waiting for an extreme risk-off scenario.

-

Expanded investable universe: From sectors to themes to market caps to debt — the fund can now participate across a much broader spectrum of opportunities in a single, managed structure.

Should You Be Worried?

For existing investors, the short answer is no — and here’s why:

- The fund’s investment objective (long-term wealth creation via thematic and sectoral rotation) remains the same.

- The expense ratio and fund management team are not changing as a direct result of this recategorization.

- The move is SEBI-compliant and investor-friendly, with greater portfolio stability built in.

- The fund continues to be classified as Very High Risk, so investors with moderate risk appetite should still assess suitability carefully.

The recategorization gives the fund more tools — it doesn’t take any away.

Key Takeaways

- Effective April 1, 2026, ICICI Pru Thematic Advantage Fund (FOF) becomes ICICI Pru Aggressive Hybrid Active FOF.

- The change is driven by a SEBI/AMFI framework for FOF schemes introduced in February 2025.

- Equity exposure shifts to 65%–80% (from 80%–100%), with a mandatory 20%–35% debt allocation.

- The fund can now take tactical market cap bets in addition to sector/theme bets.

- Core strategy — active rotation between high-conviction themes — remains fully intact.

- Debt exposure is not new; the fund has historically held 5%–17% in debt and cash.

Conclusion

Regulatory changes in the mutual fund industry can often create unnecessary anxiety for investors. The recategorization of ICICI Pru Thematic Advantage Fund into the Aggressive Hybrid Active FOF is a prime example of a change that looks bigger than it is. The fund retains its aggressive equity character, its dynamic sector rotation strategy, and its long-term wealth creation mandate — all while gaining a more robust structure and a wider investment palette.

If you’re a long-term investor who appreciated the original fund’s flexibility and thematic approach, you have no reason to reconsider your position based on this change alone. As always, review it in the context of your overall portfolio, financial goals, and risk tolerance — and consult a SEBI-registered financial advisor if in doubt.

Disclaimer: This article is for informational purposes only and does not constitute financial advice or a recommendation to buy or sell any mutual fund scheme. Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing. Consult a SEBI-registered financial advisor before making any investment decisions.

Frequently Asked Questions

What is happening to ICICI Prudential Thematic Advantage Fund (FOF)?

The scheme is being recategorized and renamed to ICICI Prudential Aggressive Hybrid Active FOF, effective April 1, 2026. This change is driven by a SEBI/AMFI regulatory framework introduced in February 2025 that requires all existing FOF schemes to align with new provisions.

Why is this recategorization happening?

On February 6, 2025, SEBI via AMFI introduced a 'Framework for launching Fund of Fund (FOF) schemes with multiple underlying funds.' To comply with this framework, ICICI Prudential is repositioning the scheme while preserving its core investment strategy.

When does the recategorization take effect?

The recategorization is effective from April 1, 2026.

Will the investment strategy change after recategorization?

No. The core strategy of actively rotating between sectors and themes remains intact. The fund will continue to focus on sectoral and thematic opportunities, preserving its aggressive equity stance.

How does the asset allocation change under the new structure?

Under the new structure, equity schemes (sectoral + thematic + tactical market caps) will constitute 65%–80% of the portfolio, debt schemes will form 20%–35%, and cash & others up to 5%. Previously, equity was 80%–100% and debt was 0%–20%.

Does the fund now have a mandatory debt allocation?

Yes. The new structure mandates a minimum 20% allocation to debt schemes, compared to the earlier 0%–20% optional range. However, the fund has historically maintained 5%–17% in debt and cash, so this is not a dramatic shift in practice.

Can the fund now invest in market cap-based schemes?

Yes. A key addition in the recategorized fund is the ability to take tactical exposure to market capitalization-based equity schemes, including small and midcap funds, in addition to sectoral and thematic schemes.

Will the fund continue to do sector and theme rotation?

Yes. Sector and theme rotation remains the primary growth engine of the scheme. The fund retains full flexibility to take aggressive or defensive positions based on the fund manager's market outlook.

Is the risk profile of the fund changing?

The fund continues to be classified as Very High Risk. While the mandatory debt component adds a layer of stability, the aggressive equity orientation is preserved, keeping the overall risk profile similar to before.

Should existing investors be concerned about this change?

No. The recategorization is a SEBI-mandated compliance exercise. The fund's investment objective, core strategy, and long-term wealth creation focus remain unchanged. The change actually expands the fund's investment toolkit rather than restricting it.

What new opportunities does the recategorized fund unlock?

The fund can now invest across a broader universe — sectoral schemes, thematic schemes, market cap-based equity schemes, debt schemes, and cash/money market instruments — giving the fund manager greater flexibility to navigate different market cycles.

Will investors bear additional costs due to this recategorization?

As an FOF, investors bear the recurring expenses of the fund of funds scheme in addition to the expenses of the underlying schemes in which it invests. This dual-layer cost structure remains unchanged post-recategorization.

0

Market insights, straight to WhatsApp — when it matters

Mutual fund updates, SIP tips, and what's moving the market. No daily noise — only when there's something worth reading.

")